Covenant Lite #12: An Introduction to NAV Lending and other Private Equity GP Solutions

Margin loans reach the private equity industry

Welcome back to Covenant Lite! We officially reached the 100 subscriber mark this week, which is very humbling. Thank you all for following this journey — I really enjoy writing this column every week and hope that you get something out of it. Reach out to say hi, if you like! I’ve already connected with many of you and get a lot out of it.

Today, I want to cover a relatively new form of private credit that is becoming increasingly topical: NAV Lending (and other forms of private equity GP solutions).

What is NAV Lending, you might ask? A NAV loan is essentially a loan made to a private equity fund secured by the fund’s investment portfolio (its NAV) rather than a single company. For my public market investors, think of a NAV loan as essentially a margin loan against a portfolio of private (as opposed to public) equity holdings. Like a margin loan, a NAV loan can enhance a portfolio’s returns when things go well — but also significantly hurt performance if used imprudently.

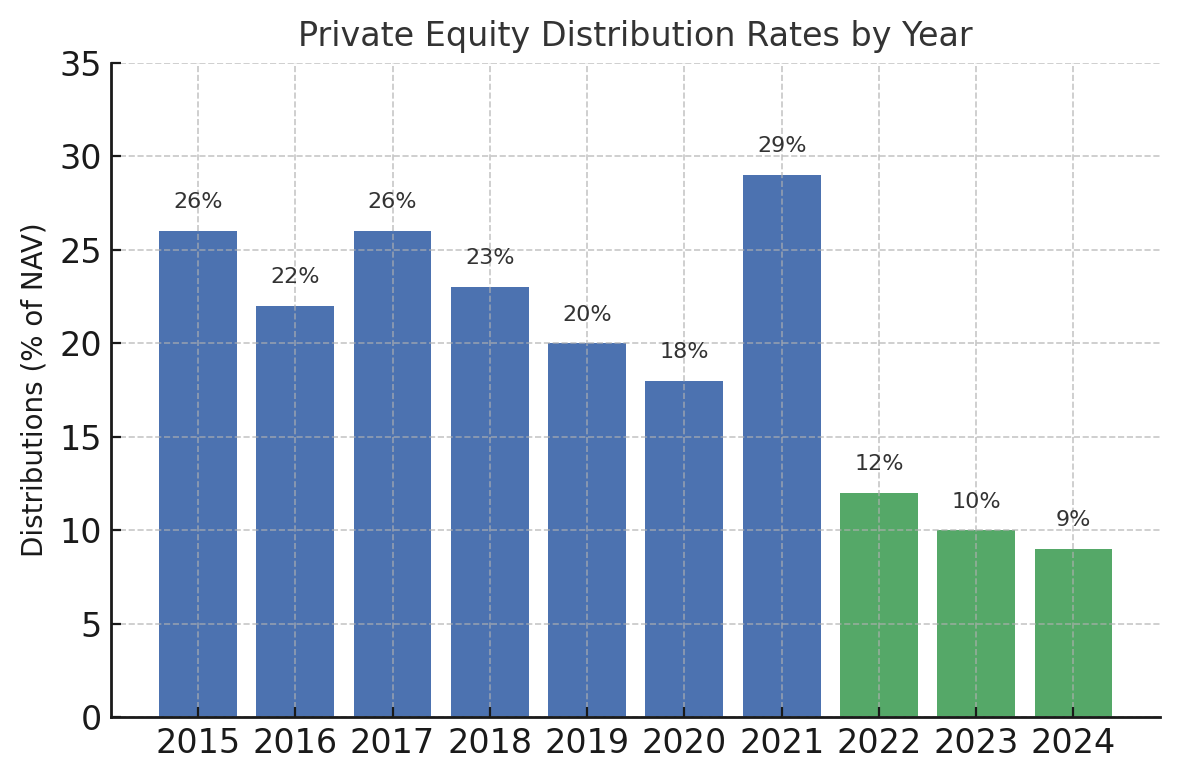

Use of NAV loans by private equity GPs has taken off in recent years for a few reasons. The biggest one is the massive liquidity squeeze facing the private equity industry. After a record surge in exit activity in 2021 — when global PE distributions to Limited Partners (LPs) exceeded $700 billion (about 29% of NAV) — payout levels have plummeted. In 2022, distributions fell to roughly 12% of NAV, 2023 saw only ~10%, and 2024 is tracking to ~9% of NAV (Link).

Source: Goldman Sachs (Link)

The big reason for these falling distributions is the rapid rise in interest rates since 2022, which increased borrowing costs and lowered asset valuations, making it harder for GPs to exit investments at attractive prices. As a result, many GPs extended their holding periods rather than sell into a weak market, throttling distributions to their LPs.

While this response may be the correct thing to do for fund returns (since it means a chance at selling for a higher price later), it has caused indigestion for LPs used to balancing new capital calls from their newer fund commitments with distributions from their old ones.

Indeed, capital calls now far outpace distributions — in 2023, new investments by funds exceeded distributions back to investors by ~80%, the widest gap since 2009 — aka the Great Financial Crisis (Link). This unprecedented cash flow imbalance has left LPs waiting much longer for returns on their committed capital and put pressure on GPs to find alternative liquidity solutions — because if they don’t, longstanding LPs may not be able to commit to the next vintage of their PE funds.

In this challenging environment, NAV Lending has emerged as a private credit tool to support PE funds. NAV Lending volume has grown dramatically in the past few years. According to leading NAV Lender, 17Capital, $44bn of NAV Loans were completed in 2023 and the industry projects $70bn+ to be deployed in 2025 (Link). Some estimates point to the market opportunity being up to $700bn by 2030, implying a lot of room for growth.

Structurally, NAV Loans are backed by a PE fund’s investment portfolio (or NAV) rather than a single company. This makes them a form of subordinated fund-level debt: the lender typically takes a security interest in the fund’s assets or a subset of holdings, but sits behind any asset-level financing in the capital structure of each equity holding.

NAV facilities are usually 2-5 year term loans designed to sunset by a fund’s end of life (or sooner if asset sales occur). LTVs are generally low — often <20% of the fund’s NAV — to give lenders a cushion against volatility at the asset level.

Interest is usually paid-in-kind (“PIK”), as opposed to cash pay, meaning that the interest accrues to the loan balance rather than being paid out in cash in quarterly or yearly installments. This is to avoid straining the fund’s cash flow. NAV Loans typically include cash sweep provisions that entitle them to a portion of the proceeds as portfolio companies generate distributions via dividends, recapitalizations or exits. The distribution percentage typically scales, with a smaller amount in the early years (say, 25%) and a larger amount (100%) thereafter until the loan is repaid.

Private equity GPs deploy NAV loans in several strategic ways to manage their funds’ liquidity and maximize investor returns:

Fund Distribution Recapitalizations: This is the topical use case right now given the lack of organic LP distributions. It involves borrowing to return capital to LPs – essentially a fund-level dividend recapitalization. Since the 1980s, buyout funds have used company-level dividend recaps (adding debt on a portfolio company to pay a dividend) to realize partial gains without selling the company. A NAV loan allows the same concept at the fund level: the GP leverages the fund’s NAV and distributes the loan proceeds to LPs as an early dividend. This can be very attractive if timed well – it pulls forward liquidity for LPs and can boost the fund’s IRR (because an earlier cash return improves IRR, all else equal).

Growth Capital for Portfolio: When a portfolio company is performing exceptionally well and needs additional capital to reach its full potential, a GP can use a NAV loan to inject new funding rather than bringing in an outside investor. This allows the fund to continue supporting winners in the portfolio (similar to how a continuation fund would, but without transferring assets) and is non-dilutive to the LPs’ equity ownership.

Rescue Financing for Troubled Assets: If a portfolio company is underperforming or in distress, a NAV facility can provide emergency capital to stabilize the business. Rather than letting a promising but cash-strapped company go bankrupt (which would impair fund returns), the GP can borrow against the broader fund portfolio and infuse rescue capital. Because the loan is secured by the diversified pool of fund assets (not just the troubled company), the financing cost is usually much lower than, say, a last-resort mezzanine loan to that single company.

As these examples show, a well-executed distribution NAV loan mainly “pulls forward” value for investors rather than creating or destroying it. LPs get cash in hand sooner, which is often welcome in a liquidity-constrained environment, and the fund’s DPI (distributions-to-paid-in) improves without materially sacrificing total return. GPs can access capital without selling assets at an inopportune time, support portfolio companies through cycles, and even deliver interim liquidity to LPs during a slow exit market.

Innovation in GP-Level Financing: Preferred Equity and Hybrid Solutions

Beyond fund-level NAV facilities, private credit is also evolving to provide capital at the GP (General Partner) or management company level. These GP-level financing solutions are often structured as preferred equity or hybrid debt-equity instruments backed by the GP’s own assets (such as future management fees, carried interest in funds, and co-investments), rather than the fund’s portfolio.

This area has expanded as GPs seek non-dilutive capital for growth and succession, in contrast to the traditional route of selling a stake in the management company. The idea is to lend against the predictable management fees and the (less predictable) incentive fees or carried interest, rather than against the fund’s assets. In practice, the GP borrows (or issues a preferred equity interest) at the management company level, gets upfront cash for strategic needs, and agrees to repay the financing from future fee revenues and carried interest distributions coming out of their funds. This effectively securitizes the GP’s diversified stream of income from multiple funds.

These facilities are typically structured as preferred equity injections or revenue-sharing loans into the GP’s holding company. Unlike NAV Loans, they often have no fixed maturity or strict covenants. The provider earns a return through a priority claim on a portion of the GP’s future economics — for example, a cut of management fees and/or carry until a target return is achieved. Because the investor’s claim is junior to fund LPs (it’s on the GP’s income, not fund assets), this capital is generally unsecured and contract-based (hence the term “soft capital” sometimes used for preferred equity).

Cost of capital for these instruments is higher than NAV Loans, typically low-to-mid teens returns, reflecting the higher risk.

Use cases for GP-level financing include:

Business Expansion and New Initiatives: GPs can raise capital to invest in their firm’s growth — e.g. seeding new fund strategies, opening new offices, or co-investing more alongside their funds — without waiting years for management fee accruals. Preferred equity injections have been used to fund platform expansion or bridge cash flow needs when launching larger successor funds. For instance, a mid-sized PE firm might use a GP financing facility to help fund its GP commitments (the 2-5% that the GP must contribute to each new fund) or to back a new strategy, rather than diluting ownership or stretching the firm’s partners’ personal finances. This enables the business to scale up faster and capitalize on growth opportunities.

Succession Planning and Generational Transfer: GP financing has become a crucial tool for succession in PE firms. As founding partners retire and transition ownership to the next generation, the junior partners often need capital to buy into the firm’s equity. Rather than forcing up-and-comers to personally finance a large buy-in (which may be prohibitive), the firm can use a structured loan or preferred equity deal to facilitate the buyout of a retiring partner’s stake. The financing provides cash to the departing founder (allowing an exit) while the junior partners can gradually pay it down via the firm’s future earnings. This approach helps transfer ownership internally without an outside equity buyer, keeping the partnership intact.

Talent Retention and Incentivization: Similarly, offering rising stars a stake in the carried interest or management company is a proven way to retain top talent – but it often requires those individuals to invest capital or pay taxes on granted equity. GP financing can be used to fund equity grants or purchases for key team members, ensuring they have “skin in the game” without undue personal financial burden. This allows the firm to lock in talent with ownership upside, which contributes to stability and investor confidence (LPs gain comfort that there is a next generation committed to the firm). In effect, the GP can borrow now to facilitate broader employee ownership and then repay from future firm revenues, aligning everyone’s interests.

In all these cases, the strategic benefit is that the GP obtains capital for long-term business needs without immediately diluting their equity or relying solely on their personal wealth. This “corporate” use of private credit at the GP level is a newer innovation, but it is growing. Sponsors continue to use preferred equity and similar structures in strategic situations – to aid fundraising, platform expansion, and cash management – and this trend is expected to increase as firms navigate the current low-liquidity cycle.

Conclusion and What This Means for Private Credit Allocators

The growing use of NAV loans and GP-level financing marks a significant evolution in how private equity is managing liquidity in 2025 and beyond. Private credit providers have stepped in to fill the gap left by slower exits, offering creative capital solutions that help bridge fundraising cycles, extend investment horizons, and support the overall private equity value creation model.

Global PE firms, large and small, are increasingly incorporating these tools to navigate the current slowdown: NAV-based lending is booming and expected to continue its rapid growth, and GP-focused capital solutions are becoming more prevalent as firms address succession and expansion challenges.

NAV Lending and GP-focused capital solutions are expected to become a larger part of the investing activities of private credit funds as firms angle to get a part of the action. Both investment types seemingly offer an attractive risk/reward profile that promises low-ish LTVs and attractive yields given the newness of the asset class.

As these types of investments become more commonplace, the yields on offer will likely come down due to competition — as we have seen in other forms of sponsor-backed direct lending. But, for now, this could be an attractive place to make an allocation and an attractive arrow in the quiver of allocators looking to diversify their private credit strategies.

Til next time.