Covenant Lite #14: Finding a common language for private credit

Ways that different data providers define private credit

Today, I thought I would try to demystify the private credit universe by exploring how leading industry players—such as Aksia, Cambridge Associates, Cliffwater, Preqin, and StepStone—break down this diverse asset class. We'll examine their frameworks side-by-side, clarifying the overlaps and differences in how each categorizes key strategies such as direct lending, mezzanine, distressed debt, structured credit, and specialty finance.

For those that don’t know, Aksia, Cambridge Associates, Cliffwater and Stepstone are leading private markets firms that research and provide advisory work on private credit funds. Preqin is one of the largest databases of private credit fund performance.

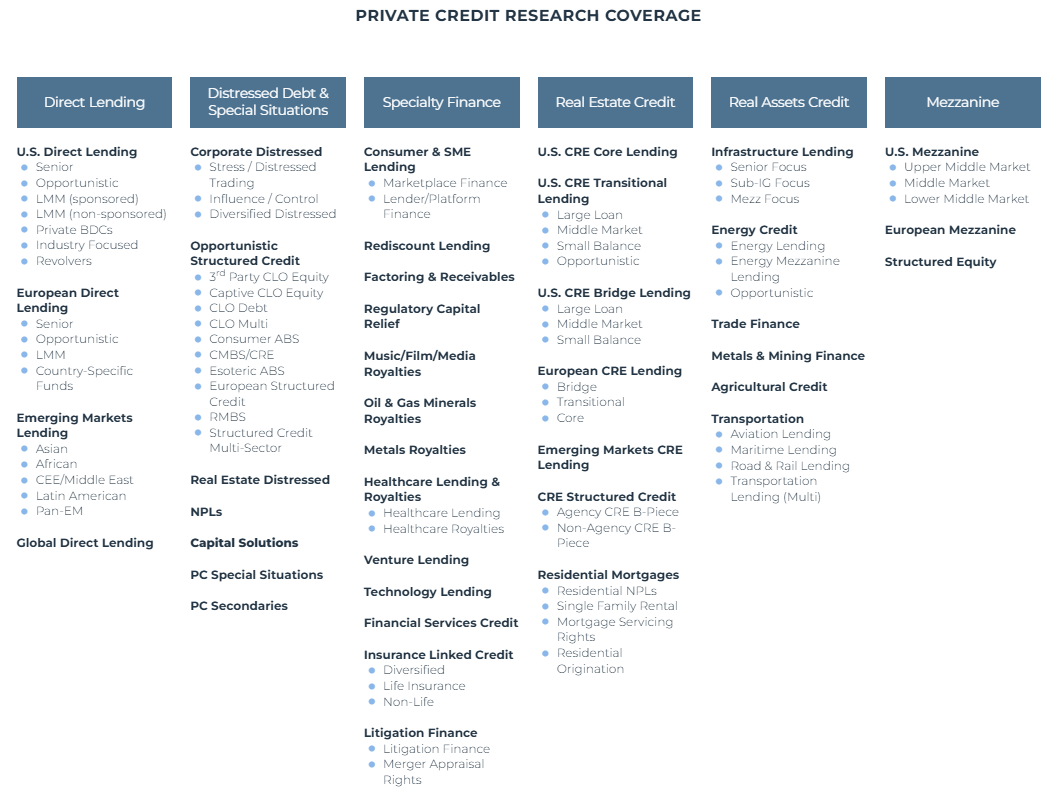

Aksia

Aksia segments private credit into several highly detailed categories (see below), notably distinguishing Direct Lending, Mezzanine, Distressed & Special Situations, Real Estate Credit, Real Assets Credit, and Specialty Finance. Within Specialty Finance, Aksia includes granular sub-strategies like consumer and SME lending, royalties, litigation finance, insurance-linked credit, and rediscount lending, clearly differentiating between traditional corporate-focused strategies and asset-backed or niche segments.

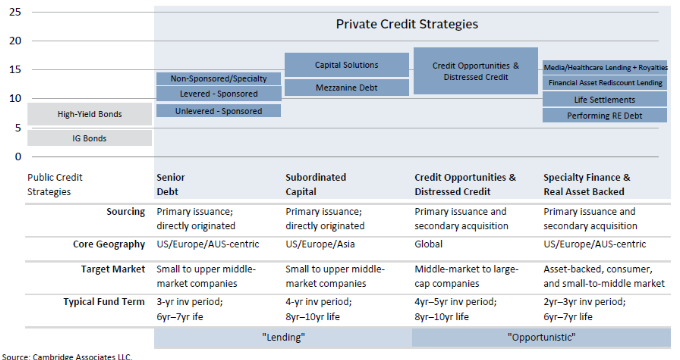

Cambridge Associates

Cambridge Associates divides private credit broadly into two main buckets: Lending and Opportunistic. The Lending category includes traditional senior secured loans (Direct Lending), subordinated capital (Mezzanine), and venture debt. The Opportunistic category comprises strategies focused on higher-risk/higher-return situations, including Credit Opportunities, Distressed Debt, and Specialty Finance, which encompasses niche asset-based or real asset-backed strategies such as royalties, litigation finance, and asset leasing.

Cliffwater

Cliffwater uses a comprehensive approach, categorizing private credit across a broad spectrum of strategies that include traditional Direct Lending and Mezzanine Debt, as well as more specialized niches such as Structured Credit (CLOs, ABS), Real Estate Debt, Infrastructure Debt, and various Specialty Finance segments (litigation, royalties, insurance-linked). Cliffwater explicitly emphasizes diversification across multiple substrategies for balanced portfolio construction.

StepStone

StepStone defines private credit through four primary corporate-oriented categories: Direct Lending, Mezzanine, Opportunistic/Distressed Credit, and Specialty Finance. Specialty Finance is broadly defined, capturing asset-based lending and niche, non-sponsor financing strategies. While StepStone acknowledges real estate and infrastructure as adjacent sectors, their core private credit categorization remains largely focused on corporate lending, distressed, and opportunistic strategies.

Preqin

Preqin focuses primarily on corporate credit strategies, explicitly identifying Direct Lending, Mezzanine, Distressed Debt, Special Situations, and Venture Debt. Unlike others, Preqin classifies Real Estate and Infrastructure Debt separately from private credit, placing less emphasis on niche specialty finance strategies within their private credit universe. Their framework closely tracks standard market conventions and emphasizes major corporate-focused lending categories.

For a simpler visualization of how each of these groups categorizes various substrategies within private credit, see below (anything marked with a black square is explicitly mentioned as a distinct substrategy by that provider):

In terms of key observations and comparisons:

Core strategies like Direct Lending, Mezzanine, and Distressed/Special Situations are consistently recognized across all major advisors.

Specialty Finance and Asset-Based strategies differ significantly in how explicitly they're called out:

Aksia and Cliffwater provide the most granular breakdown.

Preqin has a narrower focus on corporate lending strategies, excluding specialty/niche credit from its standard private debt definitions.

Cambridge Associates and StepStone have broader categories, embedding many asset-backed strategies under a "Specialty Finance" umbrella.

Real Estate and Infrastructure are explicitly separate asset classes according to Preqin, whereas Cambridge, Aksia, and Cliffwater explicitly include them within private credit.

While there are similarities, the lack of uniformity across providers speaks to one of the challenges of the private credit space: that there is not a common language to define its various components. As it evolves and matures, this is something that is going to have to change—especially as groups like BlackRock attempt to index the private markets. There needs to be a shared understanding of what constitutes private credit and where the bright lines between strategies and substrategies exist, similar to how the equity universe can be broken up into small-cap, mid-cap, large-cap or growth, value, core (blend).