Covenant Lite #24: Ozempic for Bank Balance Sheets

An inside look at SRTs: one of Private Credit's newest (and hottest) strategies

At recent private credit allocator conferences, one topic is increasingly dominating conversations—Synthetic Risk Transfers (“SRTs”). Once a niche, Europe-focused capital management tool, SRTs have exploded in global popularity, drawing attention from sophisticated allocators hungry for double-digit yields and effective portfolio diversification.

As this market evolves and spreads tighten, understanding why SRTs matter has never been more crucial. Let's dive into how SRTs went from an obscure European novelty to a booming global market—and why smart allocators are paying attention.

What Exactly is an SRT?

At its core, a Synthetic Risk Transfer (SRT) is a structured financial transaction allowing banks to offload credit risk from their loan portfolios to external investors without actually selling the loans themselves.

Here's how it typically works:

Banks select a pool of loans to reference—these could range from corporate and SME loans to residential mortgages or leases—and then establish distinct tranches of risk exposure. The tranches are designed to absorb specific loss ranges:

Junior tranche (first-loss): Usually absorbs the initial layer of credit losses, typically ranging from 0%–7% of the portfolio. This tranche offers the highest yield as it takes on the highest risk.

Mezzanine tranche: This next layer covers additional losses beyond the junior tranche, often ranging from around 7% to 10% or sometimes higher. Investors in this tranche receive moderate yields commensurate with moderate risk.

Senior tranche: The bank retains this tranche, covering losses above the mezzanine tranche’s upper limit. This layer is considered lower risk, as substantial losses would have to occur before it is impacted.

To ensure alignment of interests, banks typically retain at least 5% of the junior tranche, known as "skin-in-the-game," satisfying regulatory requirements and signaling confidence in their underwriting standards. Investors receive periodic premium payments, akin to insurance premiums, for agreeing to cover these potential losses.

By entering into an SRT transaction, banks effectively reduce their risk-weighted assets (RWAs), boosting their capital ratios without actually removing loans from their balance sheets. This regulatory benefit enables banks to free up capital, facilitating further lending and business growth.

SRT Math and Why Banks Love it

To ground the theory in numbers, let’s walk through a stylized deal. Assume a European bank holds a €2 billion portfolio of senior‑secured corporate and SME term loans.

Pre‑deal, the loans earn a standard 100 % risk weight. The bank arranges an SRT that sells: (i) a fully funded first‑loss note covering the 0‑5 % slice of losses, and (ii) an unfunded mezzanine guarantee that covers the next 3 % of losses (5‑8 % band).

Investors charge a 15% coupon for the fully-funded first-loss note and a 2% running premium on the unfunded mezzanine guarantee. Under Basel and CRR securitization rules, the portion of the portfolio protected by junior and mezzanine investors can be treated as risk‑mitigated for the originator.

Once the bank demonstrates “significant risk transfer” (usually by selling at least the first 7–10 % of loss‑bearing exposure and retaining only a capped slice), supervisors allow the remaining senior exposure to be risk‑weighted as if it were a highly‑rated securitization tranche rather than a whole loan.

That typically means a step‑down from a 100 % capital charge to somewhere between 15 % and 50 %, depending on pool type, attachment point and whether the deal qualifies for the EU’s STS label. In our example the modelled senior risk weight is 40 %, which slashes the portfolio’s RWA by 60 % even though the loans never leave the balance‑sheet.

We keep the loan margin (net interest margin, NIM) at 3 % for simplicity and assume the bank targets a 12 % CET1 ratio both before and after the trade.

As you can see above, the transaction ends up being a win-win for both the bank and the investor. The bank is able to free up equity capital that it can use to make additional loans, as well as substantially improve its ROE. Meanwhile, first-loss investors are able to earn mid-teens returns investing in a diversified pool of high quality loans.

This dynamic is why we are seeing such an increasing interest in SRT transactions from banks and (an increasingly broad swathe of) private credit investors.

How We Got Here: From Basel Experiment to Global Capital Tool

Synthetic risk transfer began life as a regulatory science project in the late‑1990s, when J.P. Morgan closed their BISTRO (Broad Index Secured Trust Offering) transaction, a synthetic CLO referencing more than 300 investment-grade corporate loans.

This transaction introduced many of the structural features that would become common to SRTs in the years to come—and proved that a bank could obtain meaningful capital relief simply by buying credit‑default protection on a reference portfolio rather than selling the loans outright.

Within a few years Germany’s state lender KfW industrialized the technique through its PROMISE conduit, syndicating billions of SME credit risk to capital‑markets investors and demonstrating that synthetics could support real‑economy lending, not just trading books.

The global financial crisis temporarily froze the market—anything labelled “synthetic” was radioactive—yet the handful of corporate and SME SRTs that existed came through 2008 with limited losses. That positive track record gave regulators the confidence to keep the door open. By 2013, with Basel III ratcheting up capital requirements, European banks rediscovered SRT as a cheaper, faster alternative to rights issues, and boutique SRT funds stepped in to buy the risk.

Despite SRTs beginning as a science project within a US bank (J.P. Morgan), European banks have dominated SRT issuance for much of the instrument’s history. In part, this is because of clearer guidance from European regulators that gave banks comfort that such transactions would earn capital credit.

SRT Issuance by Region

Source: IACPM, Seer Capital

Further clarity from the ECB and EBA in 2017 turned SRT into a repeatable playbook: clear rules on tranche thickness, clean‑up calls and retention enabled originators to execute trades year after year. Volumes exploded. Santander alone closed thirteen deals in 2018‑19, while the African Development Bank’s Room2Run transaction showed the structure could channel private capital into infrastructure and climate lending across emerging markets.

The breakthrough moment came in 2021 when the EU extended its coveted STS label to on‑balance‑sheet synthetics, trimming capital charges on retained seniors and fueling a record €145 billion of euro‑area issuance in 2022. At the same time, the U.S. Federal Reserve quietly confirmed that well‑structured synthetics would qualify for capital relief under U.S. rules, increasing adoption by US banks.

With multi‑strategy giants like Blackstone, Apollo, and D.E. Shaw now writing nine‑figure tickets, and first‑time issuers emerging in Canada, Japan and Mexico, SRT has moved from European curiosity to a core piece of global bank‑capital plumbing.

The Push-and-Pull of Supply and Demand

The SRT market is experiencing a rare two-sided expansion: banks are lining up to off-load risk just as a fresh wave of capital is eager to take it. On the supply side, euro-area issuance hit €145 billion in 2022 and has stayed above €130 billion a year since—then the United States, Canada, and Japan joined the party, adding another ~€80 billion in 2024.

Regulatory catalysts matter: Basel III “end-game” output floors, the EU’s forthcoming cut in senior-tranche risk weights, and the Fed’s 2023 FAQ have all nudged treasury desks to dust off SRT playbooks that once gathered cobwebs.

Yet demand has sprinted just as fast. A decade ago the buy-side was dominated by half a dozen London hedge-fund shops; today there are multi-billion dedicated vehicles from Blackstone, Apollo, and D.E. Shaw, unfunded guarantee desks at major reinsurers, and Dutch, Canadian, and Nordic pensions that treat SRT coupons as a floating-rate substitute for private credit. Negative yields are gone, but base rates near 5 % mean a 700-bp mezz spread still delivers a low-teens return.

This twin surge keeps pricing in an uneasy equilibrium. When Santander or Barclays brings a granular corporate pool, half a dozen investors submit term sheets and the first-loss note might clear at the tight end of the 750–850bps range. But banks that try to crowd the calendar with riskier assets—leveraged-loan or project-finance pools—still find themselves paying wide of 1 000bps.

Looking forward, the market’s balance will hinge on two numbers: (1) how aggressively U.S. regionals and Asia-Pac lenders ramp up issuance once internal capital models bite, and (2) how aggressive new entrants to the SRT space are in trying to win deals.

If both trends continue, tranche spreads could compress another 50–75bps; but if risk appetite cools—say, on a spike in default data—issuers may find they need to sweeten coupons just to clear the book.

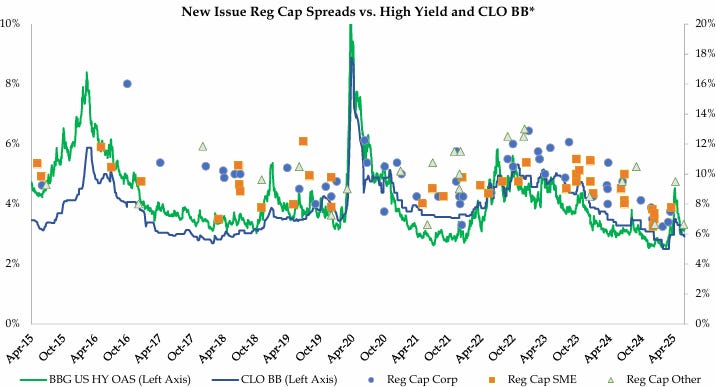

Since 2023, new issue SRT spreads have been coming down alongside other credit instruments such as High Yield Bonds and CLO BBs. However, they still offer a spread premium of 300-400bps to these more liquid options.

New Issue SRT Spreads vs. HY and CLO BB

Source: Seer Capital / Bloomberg. Reflects 1st and 2nd loss tranches.

Conclusion

Synthetic Risk Transfer began as a Basel footnote yet is now a €200‑billion‑a‑year market that blends bank‑capital engineering with genuinely attractive credit returns.

Supply is set to remain robust as Basel III end‑game rules impact U.S. and Asia‑Pac lenders, while demand is deepening beyond hedge‑fund tourists into the balance‑sheets of global insurers and pensions.

That combination has tightened spreads but still leaves investors harvesting 300‑plus basis‑points of extra carry over public CLO BBs or high‑yield—with less mark‑to‑market beta and exposure to granular, senior‑secured collateral.

As more banks and regulators embrace the structure, early adopters may find that spreads compress further in the near future. The trade is not without its risks (primarily: leverage) but may be a strategy to consider for allocators looking for premium yield.

Covenant Lite

The CRT program that Fannie Mae and Freddie Mac run are materially the same structure just using mortgages as collateral.

They offload the credit risk portion to private investors. It’s a bit uglier with mortgages and very expensive for the issuers (thus expensive for tax payers) relative to the risk.