Covenant Lite #3: An Introduction to Litigation Finance

Welcome back to Covenant Lite! For this third article on the private credit landscape, I wanted to do a deep-dive on one of the more interesting niches in private credit: litigation finance. My team has backed a number of managers in this space over time – and we continue to find it very attractive given its risk / reward profile and lack of correlation with other asset classes.

But what is litigation finance, exactly? Litigation finance, also known as litigation funding or legal financing, is when a third party, not directly involved in a lawsuit, provides capital to a plaintiff in exchange for a portion of the financial recovery from the lawsuit.

This capital can be used to cover legal expenses, such as attorney fees, expert witness fees, and court expenses. It can also be used to support working capital or personal expenses of the plaintiff. The investment is generally structured to be non-recourse, meaning the funding recipient only repays if the lawsuit is successful.

Litigation finance has grown significantly in the last decade alongside other forms of private credit, but remains a tiny portion of the overall private credit market. Per Westfleet Advisors, a leading legal advisory firm, there are 39 active litigation finance firms with a total AUM of $15.2bn as of 2023. Put in context of the $1.6trn private credit market, litigation finance hardly makes an impact.

But it punches above its weight in terms of the returns it can offer, with many funds in this space targeting net returns in the 13-15% net range – compared to 8-12% for many other forms of private credit. This return does not come without risk, of course, with certain versions of litigation finance such as single-case financing being especially risky. Increasingly, however, many of the top groups pursue investments that are more credit-oriented in nature, providing loans backed by a diverse portfolio of cases at a manageable loan-to-value (“LTV”).

Before delving more into the specifics, I thought it would be helpful to provide some historical context on the space.

A Historical Overview: From Medieval Restrictions to Modern Markets

The practice of third-party involvement in legal disputes is not new. Its origins can be traced back to medieval England, where the financing of litigation by powerful individuals led to the introduction of the doctrines of maintenance and champerty.

Maintenance, in this context, referred to the act of providing financial assistance to a litigant without having a legitimate interest in the case, while champerty involved the additional element of the third party seeking a share of any proceeds from a successful claim. These legal principles were designed to prevent the exploitation of the legal system by those seeking to profit from litigation, and they extended to other common law jurisdictions that adopted the English model (such as the United States).

The modern iteration of litigation finance began to emerge as these restrictions were relaxed or abolished. Australia played a pivotal role in this development, with a 1995 decision allowing insolvency practitioners to sell legal claims as company assets. This opened the door for third-party funding, enabling insolvent entities to pursue legal claims that would otherwise be financially infeasible. In 2006, the High Court of Australia's ruling in Campbells Cash and Carry Pty Ltd v. Fostif Pty Ltd formally recognized third-party litigation funding, solidifying the foundation for a robust litigation finance market.

In the United States, the development of litigation finance was more gradual. The widespread use of contingency fee arrangements, where plaintiffs do not need to pay legal expenses if they lose, coupled with the "American Rule" wherein each party typically bears its own legal costs, initially dampened the need for third-party funding. However, as the costs of litigation became increasingly prohibitive, particularly after the 2008 financial crisis, the necessity for alternative funding solutions became more apparent. And, today, the US market is far and away the largest for litigation finance.

The Spectrum of Litigation Finance: Consumer and Commercial Applications

Litigation finance encompasses a range of structures and applications, primarily divided between consumer and commercial contexts.

Consumer Litigation Finance typically involves non-recourse funding for individual plaintiffs with pending personal injury or similar claims. Think “slip and fall” injury cases done by firms like Morgan and Morgan. These advances provide immediate funds to cover living expenses and may be used for medical treatment or related costs. It is typically characterized by lower funding amounts, around $2,000 to $5,000. This is an area that has caused concern because of the potential vulnerability of consumers who may enter into agreements with unfavorable terms.

Commercial Litigation Finance is generally focused on funding larger business-related legal disputes, which may include contract disputes, intellectual property litigation, international arbitration, and other similar cases. The funding amounts are significantly larger, often reaching into the millions of dollars. Commercial litigation finance is further subdivided into:

Single-case financing: This involves funding for a single litigation matter.

Single-case litigation funding: Investments in individual litigations that are typically structured as a litigation funding agreement, asset-specific loan or claim purchase. These tend to be the highest octane form of commercial litigation finance with the highest potential returns (but also the highest risk).

Settlement / award monetizations or financings: Investments in court verdicts / judgments, arbitration awards or legal settlements. Because these are often de-risked, late-stage claims, they tend to be lower risk and lower return.

Portfolio financing: In this model, funding is provided for a portfolio of cases handled by a law firm or a company, allowing them to pursue multiple claims concurrently.

Law firm investments: Investment in law firms, typically structured as senior secured debt, but may include opportunistic equity and asset purchase transactions.

Corporate litigation portfolio transactions: Investments in portfolios of legal claims owned by large public or private corporations.

Legal-related specialty finance investments: Debt/equity investments in, or forward flow agreements with, specialty finance platforms that originate and/or service legal assets, including litigation funding agreements, mass tort claims and plaintiff advances.

The vast majority of private credit funds involved in litigation finance pursue commercial litigation finance given the ability to put more capital to work in the space.

Pros and Cons: Comparing Litigation Finance to Other Means of Paying for Legal Services

Plaintiffs with a claim against another party need to decide how to cover litigation costs, which may include lawyers, expert witnesses, discovery, investigation costs and asset tracing.

There are generally 3 options:

Option 1: Pay all litigation costs out of pocket. This option is the simplest, with the most potential upside since the plaintiff would receive 100% of case proceeds if they win. However, the claimant also bears 100% of the risk of losing the case.

Option 2: Contingency fee contract with law firm. An alternative to paying for ongoing legal expenses out of pocket is to enter into a contingency fee contract with a law firm. Many (but not all) law firms offer this as an option, depending on the case. The benefit for plaintiffs is that they eliminate upfront legal costs and share risk of outcomes with the law firm. However, going this route limits the choice of lawyers to only those willing to take a case on contingency. A plaintiff may also need to finance non-lawyer costs, which may be significant. The typical arrangement involves the law firm taking up to 35% of litigation proceeds.

Option 3: Litigation funding agreement with litigation funder: Engaging with a litigation funder is an attractive option for plaintiffs that want an all-in solution for lawyer fees and other litigation costs. It also enables the plaintiff the option of hiring hourly-only lawyers, who may be better equipped to handle their particular case. There is also the potential for the plaintiff to retain more upside. However, the capital is not cheap – and is most often first-out capital, meaning that the litigation funder receives a return of capital plus a multiple before the plaintiff receives anything.

Structuring Considerations: An Example of a Debt Transaction in Litigation Finance

Financing arrangements between litigation funders and their borrowers tend to be highly structured documents with specific covenants that govern the relationship. Most often, the litigation funder has a senior position which means that first loss is borne by the counterparty.

The typical approach is for the litigation funder to estimate valid damages based on case law and other factors. Often, plaintiffs will throw the kitchen sink at damages claims as a negotiating tactic and the litigation funder needs to estimate the true claim-able amount. Then the litigation funder will do an assessment of the projected recovery amount based on the specific dynamics of the case and the court where it would be tried. They then provide a loan or other form of financing at a specific loan-to-value (“LTV”) below that, often less than 50%.

In the example below, the litigation funder provides $100mm backed by $300mm of projected recoveries, for a LTV of ~33%.

The end result of this structuring by the litigation funder is an investment that should, if drafted intelligently and backed by valid cases, be fairly downside protected given its first-out status, LTVs below 50%, and the uncorrelated nature of the assets (i.e. a market crash does nothing to affect whether or not a slip-and-fall case is decided in the plaintiff’s favor).

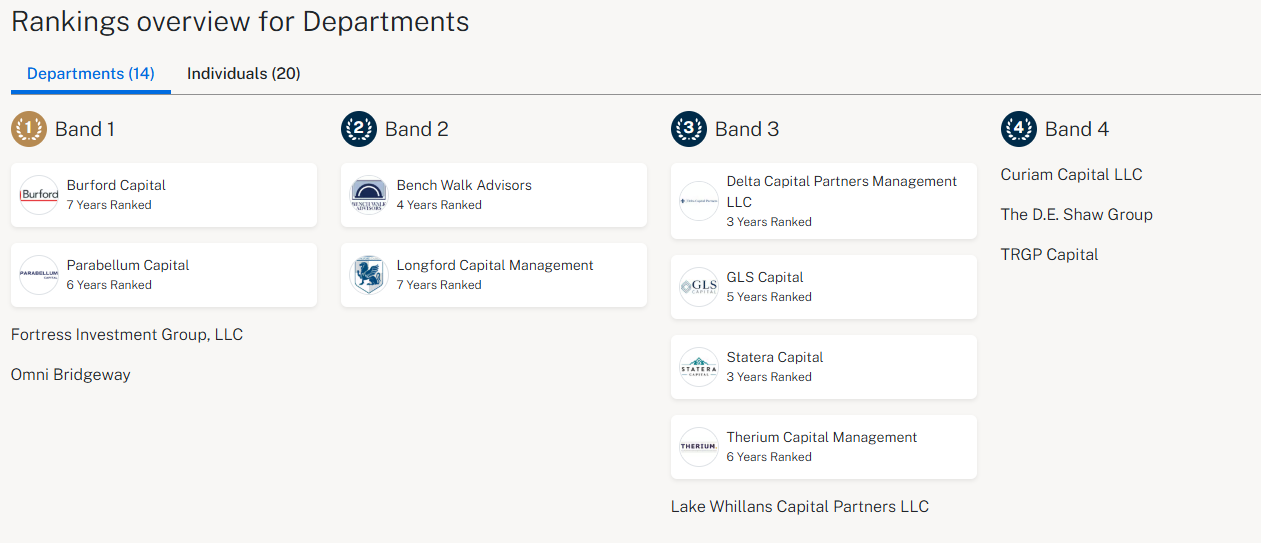

Active Players:

There are a number of well-known litigation funders in the space. Per Chambers and Partners, a leading independent professional legal research company that provides rankings of the world’s leading law firms and law firms (including litigation finance firms), the top litigation finance firms are as follows:

United States:

Europe:

This list is not exhaustive, and does not include certain smaller firms that have not paid to be ranked in this process, but provides a good overview of the more prominent groups.

Evaluating Litigation Finance Funds: A Guide for Allocators

For allocators considering investment in litigation finance funds, several factors should be considered:

Funder Expertise: Assess the depth of experience within the fund's team, with a particular focus on legal expertise and litigation experience. Teams comprising former litigators can provide a more nuanced understanding of legal risks and opportunities.

Due Diligence Process: A robust due diligence process that includes an evaluation of the legal merits, potential damages, and collectability of judgments is essential. Funders should conduct comprehensive reviews of the case, the involved parties, and legal counsel.

Transparency: Transparency in investment practices, decision-making processes, and the nature of the cases being funded is an important factor. Funds should be forthcoming with information about their investment philosophy and track record.

Deal Terms: Carefully scrutinize the terms and conditions of the funding agreement, including the funder's returns, repayment structure, and any potential limitations on claimant’s control over the litigation.

Risk Management: An effective risk management strategy is crucial, including diversification across different types of litigation and an appropriate mix of investment risk profiles. Litigation funders seek a diversified portfolio of investments that balance risk and reward.

Track Record: A proven track record of successful investments and returns provides additional support for the fund’s competency.

In addition to the above, which would be key considerations in the evaluation of any private credit fund, an allocator should also scrutinize sourcing channels and use of JV partnerships. Many of the larger groups in this space rely on these partnerships to source investments to feed their large funds. While these JV partnerships ensure that they see more dealflow, they also eat into returns for LPs since the JV partner takes a cut before the manager’s own fees. In the most aggressive cases, these relationships effectively make these firms litigation finance “fund of funds” – at least for the portion of their deals that they do not self-originate.

Conclusion: A Useful Fund Type to Consider

Like other forms of private credit, litigation finance has grown in size and stature since the financial crisis. There are now many groups that do it, but it still remains a less competitive pocket of private credit. As a result, the risk/reward in this space remains one of the most attractive in private credit - and one to consider if allocators are looking to diversify beyond more traditional forms of lending.